Math. Yup, that’s the answer. So, this authorized user tradeline concept isn’t a “chance” process. The “proof” that tradelines work is the fact that tradelines exist (explained below). The only question is how much your scores will increase. This is not a scenario in which a human being is making a risk decision or calculation. This is not a scenario in which other considerations (like income, etc.) are considered. Here’s how it works:

- Information flows into the credit bureaus.

- Credit bureau data flows through scoring models (like FICO).

- The outcome is your score.

So, when tradelines are added to your credit report, the information flows into the credit bureau(s), through the scoring models and your score is positively affected. This does assume that the tradelines added are in good standing. In fact, the federal government (well, kind of… it was the federal reserve board, which isn’t actually “federal” at all) conducted a study and concluded:

If you want to get wonky, you can check out their graph, which breaks down score changes by all types of groups (age, sex, race, etc.). However, please note that they used a Federal Reserve Board simulated score, so the score changes will be different than with FICO scores (which lenders use). Here’s the graph:

credit score changes after adding tradelinesDo tradelines always work?

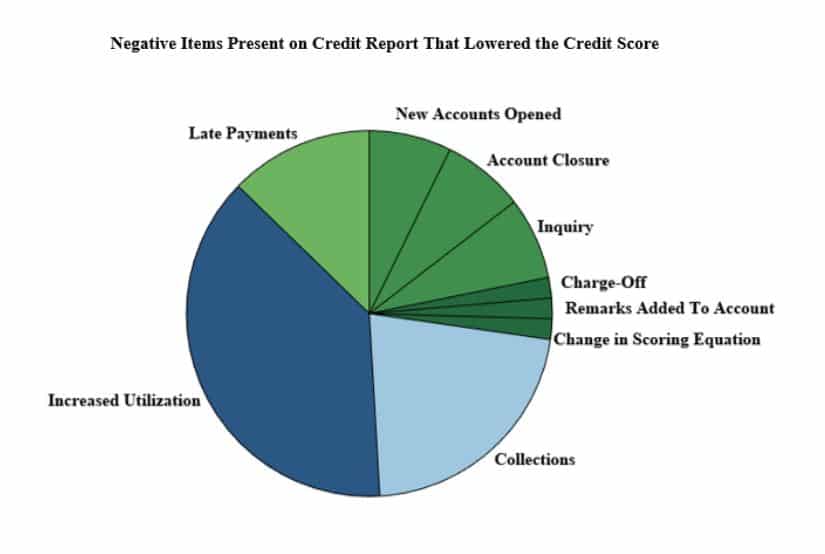

Okay, so we know that it technically works. So, how could people say it does not work? How could this go wrong? There are a couple of things that could inhibit the tradelines from improving your credit score. We recently performed a study on the benefits of authorized user tradelines which reviewed the reports of 850 participants and found the main things that kept credit scores low.

- High Utilization – Utilization accounts for roughly a third of your credit score. If the utilization is too high, then adding a tradeline will only be beneficial if it greatly reduces the utilization.

- Collections – Having recent or numerous collections can greatly reduce the impact of tradelines given how negatively these items impact your credit score.

- Recent Late Payments – Adding good payment history will only benefit you if you do not have recent late payments.

Overall, our study found that tradelines can majorly improve credit scores, in the right situation. Are you curious if tradelines are right for you? Consult with a tradeline expert to find out today!

Updated: July 30, 2021

Matias is a serial entrepreneur and CEO of many companies that help people. He owns Superior Tradelines, LLC, which is one of the oldest and most reliable tradeline companies in the country.

I purchased trade lines and when I checked my credit reports through Credit Check Total I did not see any adjustment to my scores. When I had my lender pull my reports the scores were 100+ points higher!!! Why didn’t my scores go up on Credit Check Total?

Hey Malcolm! Its a great question. This question requires a very lengthy answer, but here’s the short version. First, “lenders shall” consider authorized users. In other words, only lenders must calculate authorized user tradelines in their score (credit check total is not a lender). Second, your lender (who is a lender) pulls credit reports which comply with the Equal Credit Opportunity Act and Federal Reserve Board Reg. B., which require that lender consider authorized user accounts.

So, the answer is: Credit Check Total doesn’t have to consider the tradelines (and their impact on your score), but your lender does have to consider them… this is why your lender’s credit score report is higher (and accurate, I might add).

I hope that was helpful!

I’m having the same issue and I’m looking to lease a vehicle in the next few days but my scores are still low on Credit Karma as well as Credit Check Total. I was added to my girlfriends Barclays Credit Card and it now shows, the scores are still the same but transition went up 33points. What should I do?

It’s a good question, but can’t be answered, currently, because 1) we don’t know why your scores are low (i.e., do you have negatives, if so, what are they, how recent, how serious, etc.) and 2) we don’t know the details of your girlfriend’s Barclays account (i.e., does it have a balance, does it have a significant limit, does it have a significant age, etc.). Also, from what credit report source are you checking your credit scores? MyFico? That’s probably accurate. Everything else, not so much.

Another thing to consider is whether you’ve had an auto loan in the past, which has a disproportionate impact on your “auto enhanced” credit score.

You should rest assured about this, though: If you added a good tradeline and you have relatively limited negative items, your scores will increase (and more than what you see online).

If you want a better answer than that, the best, fastest, easiest and most accurate information will come from a credit report analysis. We do this for free. You can call us at 800-431-4741 or email us at info@superiortradelines.com or get started at https://superiortradelines.com/start to set that up.