I want a second chance at credit! I want to get a new social security number called a credit profile number or CPN because I screwed up my last one. I then want to add new tradelines of credit to create an awesome credit score. Again, I just want to start fresh!

If that sounds like you, you’re on the right page. And, there’s an awesome video, below.

The only thing worse than having no rights is exercising rights you don’t have. This is especially true when that exercise results in breaking a law. That is the risk you run when messing with CPNs.

Here’s a truth no one wants to admit. Ready?

No one understands CPNs.

100% of those interested in CPNs (whether to sell or to add tradelines to) merely recite things they’ve read online. The source of the information is usually someone else that read something online. The echo chamber has yet to produce anything that supports the concept of secondary credit.

If you truly want to understand CPNs, read on.

Good news, bad news of CPNs.

The bad news: Credit profile numbers (or “CPNs”) do not exist. It is not a real thing. This fact applies to all of the synonyms for CPNs, such as secondary credit numbers (SCNs), credit privacy numbers (also CPNs), etc. They don’t exist. You will likely break the law just trying to obtain one and you will absolutely break the law if you ever try to use one. I will prove this to you, below.

The good news: You don’t need a CPN. People run from their past rather than deal with it. If you’ve really screwed up your credit and you are drowning in debt, there are options, such as bankruptcy. You can recover from bankruptcy very quickly. If your credit isn’t that bad, then there are even easier options to recover from bad credit.

What is this page about?

There is misinformation about so-called CPNs. There are two ways that we can address them.

NOT A GOOD IDEA: We could just search the internet for all of the arguments for them and then argue against those arguments. However, that didn’t seem to work the last time we did it. People, when faced with a choice, will resort to their own beliefs (rather than facts).

GREAT IDEA: We will show you the origin of the myth of credit privacy numbers so that you can see for yourself how the law actually functions. When you understand this, you will understand why CPNs don’t exist.

Also, you will understand that trying to obtain a credit profile number (or secondary credit number) is likely illegal and using it is definitely illegal.

Finally, we will show you very simple solutions to credit problems so as to avoid the wasted time, effort and potential legal exposure associated with getting a credit privacy number (or whatever you want to call it).

Where did the CPN stuff originate?

There is a law called the privacy act of 1974. Also, there is a pervasive misunderstanding of it.

Here’s what people say the law says:

“The privacy act of 1974 says you do not have to provide your social security number and gives you a right to a credit privacy number, just like all the celebrities and rich people.”

Here’s the text of the law to which they’re referring:

“It shall be unlawful for any Federal, State or local government agency to deny to any individual any right, benefit, or privilege provided by law because of such individual’s refusal to disclose his social security account number.”

The government primarily does not grant you rights as to others. It grants you rights as to the government. Meaning, most rights granted by the government are essentially a limitation on the government’s ability to disturb your freedom.

If you want to take it one step further… Technically, the government isn’t “granting” your rights. They’re essentially saying “you’re already free to do these things and we promise not to change that fact.”

Keep reading and I promise I’ll tie this all together.

Rights, in a way, are not permissions given to you by the government. Instead, rights, in a way, are promises that the government will not interfere with your pre-existing freedoms.

For example, your First Amendment right to free speech prevents the government from censoring you (among other things). It does not prevent a private company (like Twitter or Facebook) from censoring you on their platform.

You don’t have “free speech” to walk into a restaurant and start screaming against the wishes of the owner, who, ironically, can use the power of the government to trespass you and kick you off of their property.

Here’s the point (and the most important thing you need to understand):

Congress enacted the Privacy Act to prevent the government (not private individuals or corporations, such as a bank) from abusing the collection and use of your private information.

The Privacy Act does not apply to private, non-governmental transactions. Recall that the law applies to and limits “any Federal, State or local government agency.”

James B. Lockhart, the Deputy Commissioner For Social Security, testified in Congress and stated:

“Currently, there are no restrictions in Federal law on the use of the SSN by the private sector. Businesses may ask for a customer’s SSN for such things as renting a video, applying for credit cards, obtaining medical services, and applying for public utilities. Customers may refuse to provide the number, however, the business may, in turn, decline to furnish the product or service.”

Here’s how to understand it.

In testimony before Congress about this very issue, many examples of the Privacy Act were shown. One of those examples is your right to vote. The State of Virginia tried to require the collection of social security numbers as a condition of voting eligibility.

The Court struck this down, because (now look back at the law):

It is unlawful for a State (i.e., Virginia, i.e., the government, i.e., not a private citizen or corporation, such as a bank) to deny any individual’s right (i.e., the right to vote) for such individual’s failure to provide his social security number.

Not relevant, but worth a mention.

We now know that the Privacy Act of 1974 only applies when the government is requesting your social security number. Even so, in some circumstances – which are not relevant here – the government can require that you provide them your social security number.

Here’s where the CPN theories die.

This is the best way to reword the law so it makes sense, in natural, human, everyday language:

“You lose no rights by failing to provide your social security number.”

Accordingly:

The privacy act does not apply to private transactions, such as borrowing money from a private lending institution.

You have no right, benefit or privilege to a loan from a private lending institution.

Therefore:

When a bank asks for your social security number, you must give it, otherwise;

The bank can deny your loan if you fail to give your social security number.

Finally:

If the bank asks for your social security number you provide something else, you lied.

If you lie on a loan application, that’s bank fraud.

If CPNs don’t exist (legally), how are they created (illegally)?

There are primarily two ways to create a secondary credit number and call it a CPN: Synthetic identity fraud (where you make up fake information that doesn’t already exist) and identity theft (where you use information that belongs to someone else).

Synthetic identity fraud.

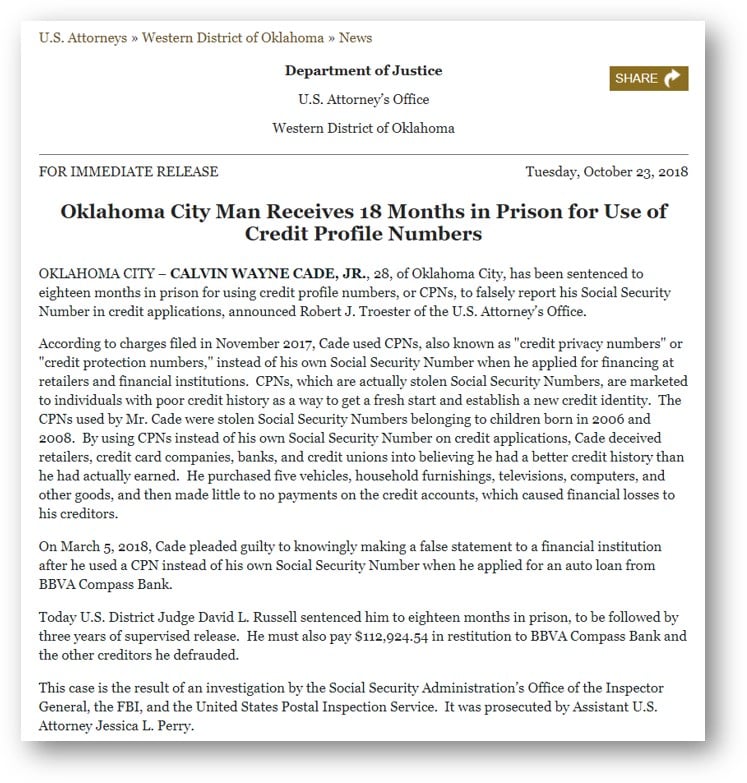

Example of synthetic identity ie CPNs being prosecuted

Here’s another example. Here’s another. Or, just go to the website for the Department of Justice and search “synthetic identity” and you’ll see all of the press releases for prosecutions.

Identity theft.

Example of identity theft ie CPNs being prosecuted

Some people go on to argue that identity theft and synthetic identity theft are not the same as using a credit profile number. Well, the Department of Justice does not agree. They recently announced the arrest of an individual for using precisely that: a “credit profile number.”

Irony.

The most ironic thing about the credit profile number shenanigans is that it relies on a law which was designed to prevent this very thing.

Remember the voting rights case discussed above? Look at the court’s reasoning:

“Since the passage of the Privacy Act, an individual’s concern over his SSN’s confidentiality and misuse has become significantly more compelling. For example, armed with one’s SSN, an unscrupulous individual could obtain a person’s welfare benefits or Social Security benefits, order new checks at a new address on that person’s checking account, obtain credit cards, or even obtain the person’s paycheck. . . . . Succinctly stated, the harm that can be inflicted from the disclosure of an SSN to an unscrupulous individual is alarming and potentially financially ruinous.”

The court is talking about why it is important that the government keep SSNs private. I.e., to prevent, among other things, identity theft. In that case, had the State prevailed, the Social Security Numbers of the voters would have been made publically available.

The main purpose of the Privacy Act is to ensure that your social security number remains private so that others cannot commit identity theft with it.

Instead, however, there are people all over the internet advocating CPNs, which – in most cases – is the procurement of someone else’s social security number. They’re taking a law designed to prevent identity theft and using it to justify identity theft.

Do you think CPNs could become legal in the future?

Actually, yes. It is possible.

In the congressional testimony mentioned above, it is clear that consumer rights advocates are actively trying to change the law. They want the Privacy Act to apply to everyone, not just the government. In other words, they want the Privacy Act to apply even in commercial transactions.

In their testimony, they specifically recommended:

“Penalize the fraudulent use of another person’s SSN but not the use of an SSN that is not associated with an actual individual. This would permit, for example, a person to provide a number such as “123-00-6789″ where there is no intent to commit fraud.”

They justified this recommendation, because:

“…consumers in the commercial sphere often face the choice of giving up their privacy, their SSN, to obtain a service or product. The drafters of the 1974 law tried to prevent citizens from facing such unfair choices, particularly in the context of government services. But there is no reason that this principle could not apply equally to the private sector, and that was clearly the intent of the authors of the 1973 report.”

This, to me, sounds like what the current CPN proponents are saying.

Here’s the problem: It’s not currently the law.

Currently, the law prohibits so-called CPNs.

Arguments made and facts to consider about CPNs.

1) What’s the actual violation of the law?

The first thing CPN advocates say is:

“CPNs are legal because there’s no law making them illegal.”

This is a very basic fallacy. Think about all the ways there are to murder someone. Do you think murder is legal if you do it creatively?

Can you find a law that says you can’t throw someone out of a plane? Since you can’t find a law making that illegal, that must be legal, right? Of course not. You would have deliberately caused the death of someone else, which is murder.

In the same way, laws against fraud do not (and do not have to) encompass every detail of a fraud’s scheme.

Most fraud laws are catch-alls.

So what laws prohibit the CPN scheme? Here’s some to name a few:

18 U.S.C. § § 1001, 1010 (HUD and Federal Housing Administration Transactions)

18 U.S.C. § 1014 (Loan and credit applications generally)

18 U.S.C. § 1028 (Fraud and related activity in connection with identification documents)

18 U.S.C. § 1341 (Frauds and swindles by Mail)

18 U.S.C. § 1342 (Fictitious name or address)

18 U.S.C. § 1343 (Fraud by wire)

18 U.S.C. § 1344 (Bank Fraud)

42 U.S.C. § 408(a) (false social security number).

…among others.

You could potentially commit tax evasion, too. Why? Because if you have income on two different social security numbers, you could potentially offset your tax bracket, illegally, by splitting your income over two different numbers.

2) I am permitted to provide something other than my social security number.

CPN advocates claim, through an impressive logical leap, that:

“You are not required to provide your social security number, so it’s not fraud when a bank asks for it and I provide something slse.”

First of all, this argument relies on the Privacy Act. However, this is absolutely not what the law says. The law says you don’t have to give your social security number to a government agency (except for a few circumstances). You have absolutely no right like this when contracting with a private individual or company.

You can absolutely not give your social security number to a private entity. In exchange, the private entity can refuse to work with you.

Let’s say you did have a right to not provide your social security number (which you don’t):

Where in this law does it say you can create and provide a number other than your social security number?

It doesn’t.

3) I am entitled to a CPN to protect myself from identity theft.

More arguments go like this:

“I want to protect my identity by having a separate and secret CPN other than my SSN.”

The craziest part about this identity theft argument is that obtaining a CPN is usually identity theft in and of itself. So, they’re saying “I can commit aggravated identity theft using someone else’s social security number just in case someone else commits aggravated identity theft against my social security number.”

In addition, if someone can steal your social security number, why can’t they steal your credit privacy number?

You have no such right and, even if you did, it is logically flawed and ineffective.

What to do instead of CPNs.

We can’t speak for the motives of those selling CPNs. Some may be good people that simply misunderstand what they’re doing. Others may have full command over the fraud they’re committing.

What is for sure: If you get a CPN, you are victimizing yourself. You now know better.

What’s more: There are alternatives.

I know of no person in human history who’s credit and financial situation cannot be solved (unless you’re talking about backward societies with debtor jails). In the United States, there are all sorts of laws and private entities capable of helping you.

There’s credit repair.

There’s debt settlement.

There’s bankruptcy.

There’s a huge list of consumer protection laws.

There are tradelines.

The CPN challenge.

Call us. See if we can propose a solution for your current situation.

Without a doubt, we will provide a better way than CPNs.

16 thoughts on “CPN and tradelines: Understanding what you can and cannot do.”

My credit score is 540ish by next month I should have 0 debt, but I want my credit score above 750 by year end. What’s the best solution for this. Trade lines? And how much does the service cost to do something like this. I’m trying to buy my first house but I want the best Interest rate.

If you need to boost your credit score fast with tradelines, that’s a possibility. However, this is not a product which applies in all circumstances. For example, if you have actively reporting collection accounts, the trade lines are to help you. If you have this significantly more negative items than positive, the trade lines are to help they might not over, the deficiency you face in terms of credit. Or other examples include situations in which your credit score and qualify you for a loan, but some particular account or issue in your credit report would cause an automatic denial during underwriting.

So, if you need to boost your credit score fast with tradelines, you need to consider the totality of the circumstances of your credit file. This can be done by a free credit report analysis by one of our trained experts. We will go through your credit report, line by line. We will ask what your goal is. And from there, will determine whether or not trade lines are a viable option to achieve your goals.

Tradelines are not for everybody or every credit situation, but if you are a potential candidate, will certainly let you know. If we tell you that trade lines are not going to work, you should highly consider our recommendation for alternative methods of credit enhancement, such as credit repair. We want to make sure our services work for clients, sore not to waste time trying to shove around peg in a square hole. If you need to boost your credit score fast with tradelines, let us perform a credit report analysis and help you determine whether tradelines are right for you.

All great Information. But while we are at it, lets be clear!!!! Trades are not guaranteed to work either. Some wont post and some can even drop your credit score. So if we are going to talk cpns lets talk all the way around the board. Some Chase accounts used to piggy back have to be crossed addressed with the same address of the Primary account holder. You spend 3000 for good seasoned tradelines that may fall off in 30-45 days if you dont purchase the extension offered , and watch the 20-200 point increase fall right off your credit report. So lets be all the way transparent here.

How do I fix it if I got scammed and a “credit repair” company opened credit lines for me using a CPN? If I call the credit card companies and give them my correct information are they going to have me arrested?

We would recommend you close out the CPN and ask the company or person you got it from for a refund. Then, stay away from CPNs and count your blessings that you didn’t get flagged for any kind of fraud or other issues. If you need help with your credit, we’d be happy to discuss.

Im opening up a new business and I dont have any established credit with the business and dont want my SSN attached. What do you think is the best approach to establish credit fast?

My brother is being released from prison soon and I want to know what we can do to get him started on the right foot credit wise so that he can become financially stable shortly after his release. He’s been gone 10 years and I’m curious if the inactivity is good or bad for him and if his criminal record will effect his credit coming out?

You have rights under the law and, unlike other companies, we tell you about them so you can exercise them. By creating an account on our website through any sign-up form or any other method, you expressly consent to Superior Tradelines, LLC, it’s employees, contractors, agents and assigns (hereinafter “our” or “we”) communicating with you, using any phone number, including a mobile or cell phone number, or email address that you have provided us using any current or future means of communication at our full discretion and transmitted by any available means. Technologies we may use to contact you include, but are not limited to, automatic telephone dialing equipment, artificial or pre-recorded voice messages, SMS text messages, or email, all of which may be transmitted by any available technology. YOU ACKNOWLEDGE THAT YOU MAY INCUR COSTS FROM YOUR SERVICE PROVIDER RELATED TO RECEIPT OF OUR COMMUNICATION AND YOU FURTHER CONSENT TO USE OF THESE MEANS OF COMMUNICATION EVEN IF YOU INCUR COSTS. You understand that you may revoke your consent to receive communication from us by visiting: https://members.superiortradelines.com/opt-out You also understand that it may take up to 48 hours before Superior Tradelines, LLC can acknowledge your revocation of consent.

My credit score is 540ish by next month I should have 0 debt, but I want my credit score above 750 by year end. What’s the best solution for this. Trade lines? And how much does the service cost to do something like this. I’m trying to buy my first house but I want the best Interest rate.

Email me, I want to get started

CPN’s been around a long time.

I need 2 cpns how much it’ll cost me

Please help. I need to boost my credit score fast with tradelines.

If you need to boost your credit score fast with tradelines, that’s a possibility. However, this is not a product which applies in all circumstances. For example, if you have actively reporting collection accounts, the trade lines are to help you. If you have this significantly more negative items than positive, the trade lines are to help they might not over, the deficiency you face in terms of credit. Or other examples include situations in which your credit score and qualify you for a loan, but some particular account or issue in your credit report would cause an automatic denial during underwriting.

So, if you need to boost your credit score fast with tradelines, you need to consider the totality of the circumstances of your credit file. This can be done by a free credit report analysis by one of our trained experts. We will go through your credit report, line by line. We will ask what your goal is. And from there, will determine whether or not trade lines are a viable option to achieve your goals.

Tradelines are not for everybody or every credit situation, but if you are a potential candidate, will certainly let you know. If we tell you that trade lines are not going to work, you should highly consider our recommendation for alternative methods of credit enhancement, such as credit repair. We want to make sure our services work for clients, sore not to waste time trying to shove around peg in a square hole. If you need to boost your credit score fast with tradelines, let us perform a credit report analysis and help you determine whether tradelines are right for you.

All great Information. But while we are at it, lets be clear!!!! Trades are not guaranteed to work either. Some wont post and some can even drop your credit score. So if we are going to talk cpns lets talk all the way around the board. Some Chase accounts used to piggy back have to be crossed addressed with the same address of the Primary account holder. You spend 3000 for good seasoned tradelines that may fall off in 30-45 days if you dont purchase the extension offered , and watch the 20-200 point increase fall right off your credit report. So lets be all the way transparent here.

Totally agree. We just posted a 24 page study that took over a year to compile which covers everything you mentioned and more:

https://superiortradelines.com/study/

How do I fix it if I got scammed and a “credit repair” company opened credit lines for me using a CPN? If I call the credit card companies and give them my correct information are they going to have me arrested?

cpn

I’ve got friend that used cpn and is it possible to get one ?

Did you get your question answered?

My cpn and tradeline doesn’t work. What now

We would recommend you close out the CPN and ask the company or person you got it from for a refund. Then, stay away from CPNs and count your blessings that you didn’t get flagged for any kind of fraud or other issues. If you need help with your credit, we’d be happy to discuss.

Im opening up a new business and I dont have any established credit with the business and dont want my SSN attached. What do you think is the best approach to establish credit fast?

My brother is being released from prison soon and I want to know what we can do to get him started on the right foot credit wise so that he can become financially stable shortly after his release. He’s been gone 10 years and I’m curious if the inactivity is good or bad for him and if his criminal record will effect his credit coming out?