Most people think adding any tradeline will boost credit scores. The truth is, choosing the best tradelines depends on your credit profile’s unique factors like payment history and account age. This guide breaks down how seasoned authorized user tradelines impact your credit report and shows you how to pick options that fit your goals. Keep reading to understand realistic timelines and steps toward stronger credit profile strength. For more insights, visit this resource.

Table of Contents

Understanding Tradelines and Credit Scores

Understanding how tradelines impact your credit score can unlock opportunities for financial growth. Tradelines, simply put, are accounts that appear on your credit report. They document your borrowing and repayment behavior, which significantly influences your credit score. Knowing how tradelines work is the first step in improving your financial standing.

Impact of Tradelines on Credit

Tradelines can make a big difference in credit scores by showing payment history and available credit. When you have a tradeline, it reflects your credit behavior to lenders. This history can either boost your score if managed well or hurt it if mismanaged. For example, a positive payment history on a credit card as an authorized user can improve your creditworthiness. On the flip side, negative history can pull your score down.

Types of Tradelines Explained

There are different types of tradelines, and each affects your credit score in unique ways. The primary types include installment and revolving tradelines. Installment tradelines include loans you repay over time, like car loans or mortgages. Revolving tradelines, like credit cards, allow you to borrow up to a limit and pay it back flexibly. Understanding these types helps you choose the right ones for your credit goals.

How Tradelines Affect FICO Scores

Your FICO score is influenced by several aspects of tradelines. Payment history and credit utilization ratio are major factors. A well-maintained tradeline with timely payments can positively impact your FICO score. Conversely, high credit utilization suggests risk, potentially lowering your score. Regularly monitoring these aspects can help you maintain a healthy credit profile.

Choosing the Right Tradelines

Selecting tradelines that fit your credit profile is essential for optimizing your score. Knowing what to look for in a tradeline can help you make informed decisions. Let’s explore how to identify the best tradelines for your needs.

Identifying Best Tradelines

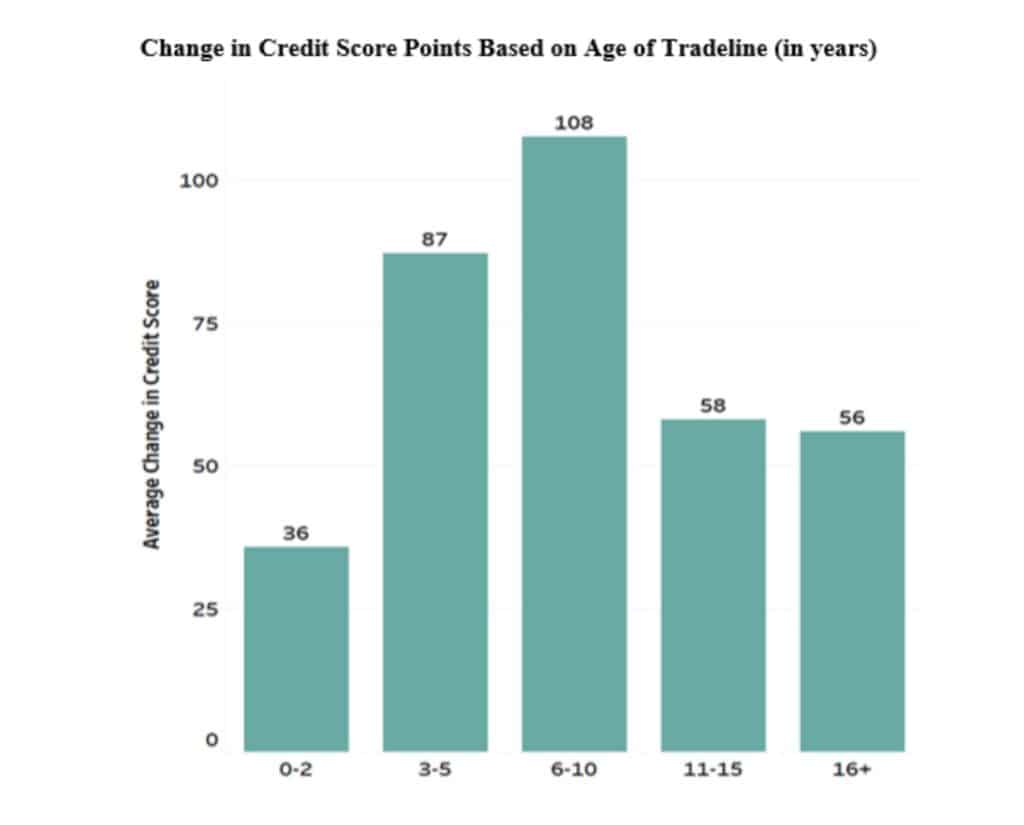

To find the best tradelines, look for those with a strong payment history and low credit utilization. Tradelines that have been active for six to ten years often yield better outcomes. It’s also beneficial to choose tradelines with positive histories and low balances. These factors contribute to a more favorable impact on your credit score.

Primary vs. Authorized User Accounts

Primary accounts are those in your name, offering more impact on your credit score. Authorized user accounts, on the other hand, allow you to benefit from someone else’s credit history. While primary accounts carry more weight, becoming an authorized user can still enhance your credit profile if the primary user has a strong credit history.

Evaluating Tradeline Reporting Dates

Timing matters when evaluating tradeline reporting dates. You should examine when the tradeline was opened and its reporting history. Tradelines that report consistently over time show reliability. Pay attention to when updates appear on your credit report too, as this affects how quickly you’ll see changes in your score.

Building a Strong Credit Profile

Building a robust credit profile requires more than just adding tradelines. It involves managing payment history, credit utilization, and the average age of accounts. Let’s delve into how you can strengthen these areas.

Importance of Payment History

Payment history is crucial in credit scoring. Lenders want to see consistent, timely payments. A history of late payments can severely impact your credit score, while a clean record boosts it. Aim to pay all bills on time to maintain a positive payment history.

Managing Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’re using compared to your limit. Keeping this ratio low, ideally below 30%, is important for a healthy credit score. High utilization suggests financial stress, which can lower your score. Regularly monitoring and managing this ratio is key to maintaining a strong credit profile.

Average Age of Accounts and Credit Score

The average age of your accounts also affects your credit score. Older accounts positively influence your score as they show long-term credit management. Having a mix of older and newer accounts can help balance your credit profile.

Get Expert Help and Support

Sometimes, navigating credit complexities requires expert guidance. Superior Tradelines offers support tailored to your credit needs, ensuring you make informed decisions.

Book Your Complimentary Consultation

Don’t navigate the credit maze alone. Book a complimentary consultation to explore personalized solutions for your credit score challenges. This session is designed to assess your situation and offer tailored guidance.

Personalized Tradeline Fit Plan

Receive a personalized plan that matches your unique credit profile. This approach considers your goals and provides actionable steps to enhance your credit score. Let experts guide you toward achieving the credit health you desire.

Superior Tradelines: Trusted Credit Education

Superior Tradelines is your trusted source for credit education. With over 15 years of experience, we prioritize transparency and professionalism. Our educational resources empower you to make informed decisions about your financial future.

🌟📈

Frequently Asked Questions

What is a tradeline on a credit report?

A tradeline is a record of credit activity for an account, showing your borrowing and repayment history. This information is used by lenders to assess creditworthiness.

How do tradelines affect credit scores?

Tradelines impact credit scores by showing payment history and credit utilization. Positive tradelines can boost your score, while negative ones can lower it.

What is the difference between primary and authorized user accounts?

Primary accounts are held in your name and have a greater impact on your credit. Authorized user accounts allow you to benefit from another person’s credit history.

How can I choose the best tradelines for my credit profile?

Select tradelines with a long, positive history and low balances. Look for seasoned tradelines, ideally active for six to ten years, to maximize impact.

Why is payment history important for credit scores?

Payment history is a major factor in credit scoring, reflecting your reliability as a borrower. Consistent, on-time payments positively influence your score.