We get asked about buying business tradelines all the time, and the answer isn’t as simple as you might think.

Table of Contents

BUSINESS TRADELINES… OR TRADELINES FOR BUSINESS?

Before we get started, let’s clear one thing up – we are not here to try and sell you business tradelines. People tend to be somewhat misguided about this topic, so we feel it’s important to clear up common misconceptions about the practice. Our goal is to help get you pointed in a better direction that will help you reach your goals with far less risk and hassle.

The short answer is no – you can’t buy tradelines for your business. Business tradelines are different from personal tradelines. You can, however, buy authorized user tradelines to boost your personal credit score, in order to get in a better position to guarantee a business credit card.

This is probably going to be the most direct way to achieve your goals. You can’t circumnavigate a poor personal credit score by using your business credit line. If you’re looking to secure business lines of credit for loans or funding, there are better ways than purchasing business tradelines.

WHAT IS A TRADELINE?

Tradelines, in the most general terms possible, are accounts in your credit report. “Tradeline” means “account”, and businesses have “accounts”, so yes, technically businesses have “tradelines.” They can also refer to the various accounts on your personal credit reports.

Ever since the Equal Credit Opportunity Act passed in 1974, people have been able to buy authorized user tradelines, or seasoned tradelines. This is to boost their personal credit score by becoming an authorized user on someone else’s credit card with a good credit history and better credit score than them.

That person – with the higher credit score – is called the primary account holder. Any activity on their account affects the authorized user’s personal credit scores, for better or for worse.

WHY WOULD SOMEONE WANT TO BUY BUSINESS TRADELINES?

There are typically two reasons why an individual might be looking for tradelines for their business. One reason is that they are looking to get business loans and want to improve their chances of securing a loan.

But the most common reason we see is that people often think that they can circumnavigate their bad personal credit line by using the credit from their business instead.

WHY SUBSTITUTING BUSINESS CREDIT SCORE INSTEAD OF PERSONAL CREDIT SCORE DOESN’T WORK

Unfortunately, within the scope of the law, it is very difficult to bypass your bad personal credit by simply signing up for a business credit card.

It is not possible to buy business tradelines in the same way an individual can buy authorized user tradelines. In order to apply for business credit cards in the name of the business, the individual applying will have to have sufficient credit capacity. So if you have a poor credit score, you will probably not even be able to qualify for a business credit card in the first place.

A more legitimate option would be to purchase authorized user tradelines and begin working on improving your personal credit score. Why? This is a more legitimate way to get a business line of credit based on your personal credit. By improving your personal credit score, you are in a better position to qualify for business loans and credit cards.

Really, there aren’t many legitimate options other than repairing your own personal credit. That’s not necessarily a terrible thing.

Repairing your credit will position yourself to personally guarantee a line of credit for your business. That is the best and most reliable way to achieve your financial goals.

TRADELINES FOR FUNDING, LOANS OR CREDIT CARDS

If you’re actually trying to build your business’s credit history by adding tradelines to your business credit report, there are companies that specialize in helping you do so. Getting bank approval for loans is extremely difficult for small businesses. There are companies that can help you establish paperwork, banking relationships, and transactions in commerce to show business credit agencies that the business is successfully operating and has a positive payment history. However, you’ll pay for the service.

Most banks do not currently lend business loans without some kind of personal guarantee. Also, businesses usually can’t get backed up without good personal credit in the first place.

Usually only huge corporations with millions of dollars in revenue, like SpaceX or Amazon, get approved. Capital requirements are usually insane, which is one of the reasons only large corporations are able to do it.

This is often counterintuitive, because the businesses that truly need the loans are the ones that are struggling, or are new and don’t have a credit line established. Occasionally, a business might be lucky enough to be able to procure an investor, but these opportunities are few and far between. It’s better to explore legitimate options, rather than go down the Google rabbit hole which can lead you into all kinds of tricky situations.

So, how else can you get a business loan? Connect with somebody with experience. This can save you a ton of time by doing things correctly. They may know tricks and techniques to help expedite the process, avoid mistakes, and be more efficient.

We recommend checking out the following experts who can get you pointed in the right direction:

This is an organization dedicated to alternative business funding. From their website, “Over 90% of business loans come from alternative lenders, not conventional banks.” If you are genuinely interested in obtaining a business loan, this is a great place to learn more information.

Ty Crandall is an expert in building business credit and everything that goes along with it. We recommend checking out his website as it’s a great resource for anyone looking for more information about business credit scores or financing.

Remember, borrowing money is the opposite of making it.

If you can meet the requirements to qualify for a business loan, you probably don’t need one. It is our opinion that it is usually not is a business’s best interest to take out a loan. There are usually better options available, if you’re willing to think outside the box.

CAN’T I JUST BUY PRE-EXISTING BUSINESS LINES OF CREDIT?

This is a common misconception. You may have heard of the term “shelf corporations”. These are pre-established business entities that are left to sit on the “shelf” to age without generating any financial activity.

SHELF CORPORATIONS & ASSUMABLE ACCOUNTS

They were essentially assumable accounts where one would assume responsibility for a pre-existing line of credit through the shelf corporation. Then the people selling it to you would charge you for the service.

This is a very murky area, legally speaking. In order to do it correctly it is a very sophisticated and complicated process. That meant that it was difficult to make the process profitable, and consequently people started cutting corners. This resulted in legally compromised products, fake documents, fraudulent behavior, and so on.

The supposed benefit of shelf corporations was that you were more likely to get better Paydex scores and funding from banks, but that has proven to be untrue in the vast majority of circumstances. As a result, shelf corporations have become predominantly unnecessary. They may still exist, but there are far better options.

BEST OPTIONS FOR INCREASING BUSINESS CREDIT SCORE.

All right, so by now hopefully we’ve drilled it into your head that you can’t buy authorized user tradelines for your business in the same way you can for your personal accounts. So if you are trying to build your business credit, you are probably wondering what are my options for increasing my business score, then?

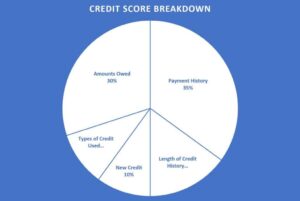

It’s important to have a good business credit score because this is how banks and lenders determine whether or not a business can be relied upon to settle its debts in a timely manner. Unfortunately, there is no exact science when it comes to raising one’s credit score, because it can be incredibly complex to determine. But there are several ways that you can help influence your credit score positively over time, or better yet, prevent it from dropping too low in the first place.

FIRST, ESTABLISH CREDIT WITH COMPANIES THAT REPORT TRADE INFORMATION.

Like the catch 22 in personal credit, you need business credit to build business credit and you need established business credit to get business credit. One of the ways to do that is to get some kind of account that reports to business credit bureaus. For example:

Net30 accounts.

Government loans (like EDIL, PPP, SBA, etc.)

ALWAYS, ALWAYS PAY BUSINESS BILLS ON TIME.

One of the most reliable ways to ever prevent your credit score from dropping in the first place (and, in fact, to make them go up) is to pay your bills on time. Think about it – the practice of lending money is incredibly risky. Just like the saying goes, don’t ever let anyone borrow anything that you wouldn’t be okay with not getting back.

Banks and lenders have made the practice of approving businesses for loans lucrative. That means taking measures to ensure that they’ll actually be paid back.

By paying your bills on time, you’re communicating that you can be trusted to hold up your end of the bargain. That means it’s more likely that banks will lend to you. A few tips to make this easier are:

Set up alerts and email reminders for all of your bills.

Sign up for auto payments whenever possible.

Set reminders on your phone.

Leave notes for yourself (if you’re old school).

DON’T BE SCARED TO CHECK YOUR CREDIT REPORT (AND BANKING STATEMENTS) REGULARLY.

Negative activity on your personal credit report could affect your business credit score negatively. It’s important to know exactly what is on there.

It’s possible to get certain items removed from your credit report if you are able to dispute them. Communicate with credit reporting agencies if you believe you see something on your credit report that doesn’t belong there.

For example, maybe someone stole your credit card and racked up a bunch of charges. You should be able to dispute that with your credit reporting agency. However, you will have to provide proof of fraudulent activity.

OPEN MORE LINES OF CREDIT.

Certain vendors are able to provide lines of credit to their customers. This is usually through major corporations such as Amazon, Apple, or Uline.

If you work with any of these suppliers on a regular basis, there may be benefits to opening a business credit card account with them. For example, Amazon offers 5% back on all purchases made with an Amazon card through their app. Different corporations offer different benefits for using their credit services, so think about what benefits you need the most.

Furthermore, even if you get approved for more credit than you need, not using all available credit to you is a green flag for credit reporting agencies. This shows them that you’re not strapped to your limits and are able to balance your financial demands.

On the flip side, don’t get more credit than you can handle. It’s important to be diligent about your credit accounts and having too many at once can be difficult to manage. You don’t want to end up using more credit than you can pay off.

IF YOU ARE STRUGGLING TO INCREASE YOUR BUSINESS CREDIT SCORE, WE CAN HELP.

We know that it is far too easy to drown in the endless sea of options out there and lose sight of your goals. If you’ve researched this far, it shows that you have probably looked into every available option, but perhaps sometimes it’s best to zoom out and rethink your goals. Sometimes it may not even be in a business’s best interest to seek funding when there are other options, such as looking into generating more revenue instead, for example.

Sometimes your best option may be right in front of you without even realizing it. Talking to a professional can help streamline the process by getting you in touch with the appropriate resources to help solve your problems.

We’ve already done all the research, why not spare yourself endless hours on the internet trying to figure out what to do next by talking to one of our trusted advisors?

FREQUENTLY ASKED QUESTIONS

1. DO BUSINESS TRADELINES EXIST?

In a sense, yes, but probably not in the way you’re thinking. Tradelines mean “accounts” and business have “accounts” so yes, technically there are business tradelines. However, they do not exist in the way authorized user tradelines exist for personal accounts.

2. CAN I PURCHASE BUSINESS TRADELINES?

No. Business tradelines do not work in the same way as personal tradelines. You can, as a substitute, purchase authorized user tradelines for your personal account and begin repairing your credit score in that way. Then you may be eligible in the future to qualify for business loans, funding, or credit cards if the banks rely on your personal credit in order to lend to your business.

3. WHAT IS THE DIFFERENCE BETWEEN BUSINESS TRADELINES AND AUTHORIZED USER TRADELINES?

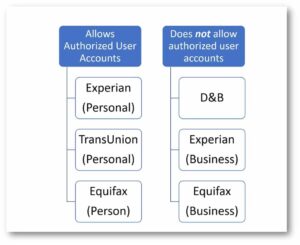

A business tradeline is an account that a business would report to a credit agency such as Experian, Equifax, or Transunion. This would include things such as business credit cards or vendor accounts. Authorized user tradelines refers to the practice of becoming an authorized user on someone else’s account in order to increase your credit score. You cannot buy authorized user tradelines for businesses in the same way that you can buy authorized user tradelines for your personal credit score.

4. HOW MUCH IS IT TO BUY BUSINESS TRADELINES?

Again, you cannot buy business tradelines… However, authorized user tradelines for your personal account can run anywhere from a hundred dollars to several thousand, depending on your needs. It is best to talk to a professional consultant in order to determine the right amount of money to spend.

5. WHAT ARE SEASONED OR AUTHORIZED USER BUSINESS TRADELINES?

This is a common misconception – first of all, seasoned tradelines and authorized user tradelines are the same thing. They apply strictly to the personal side of your credit score. You cannot buy seasoned or authorized user tradelines for businesses in order to increase a business credit score. You can, however, buy them to increase your personal credit score.

6. IS IT POSSIBLE TO ESTABLISH BUSINESS CREDIT WITHOUT PERSONAL CREDIT?

Yes, it just takes forever. Banks have slammed on the breaks in terms of “business loans.” In fact, most banks won’t lend to you at all unless you have $5,000.000.00 in revenue. Contrary to this, in a way, the government does – sometimes – create programs to help fund business which “promises” the bank that the government will repay the loan if you do not. This could be a standard SBA loan, or special programs such as those that originated during Covid-19, such as EDIL, PPP, etc. Again, talking to a professional skilled and experienced in this area is your best bet.

This is why most business funding experts have focused their efforts on unsecured business lines of credit. These lines of credit are basically a credit card in the name of the company. The credit cards rely on the business owner’s (or signer’s) personal credit, rather than the business’s credit. This is the main way the business tradelines are created these days.

7. HOW MANY TRADELINES SHOULD A BUSINESS HAVE?

The Dun & Bradstreet Paydex scoring model (or DUNS number) requires at least two tradelines, and in some cases three, before your business is eligible for a credit score.

8. IS IT LEGAL TO BUY TRADELINES?

Yes, it is legal to purchase authorized user tradelines for your personal credit accounts, however, it is not possible (or legal) to buy business tradelines because it simply doesn’t work that way. Beware of anyone telling you otherwise.

9. ARE THERE BUSINESS TRADELINES WITH NO UPFRONT FEE?

No, there is no such thing as buying business tradelines, therefore, there is no such thing as buying them with no upfront fee. Typically you’ll see websites using this term as a form of “clickbait” knowing it’s what you want to hear. For example, some companies might say they offer tradelines with no upfront fee, and what they’re really saying is they’ll help you get them and then charge a fee for it later. Sneaky, sneaky!

The true way to make sure you don’t pay upfront for fees is to use an escrow system, like Credzu. Be sure to use escrow if you are going to buy anything in the personal or business credit or debt space.

10. WHERE CAN I GET A LIST OF TRADELINES FOR BUSINESS?

Business tradelines are accounts that you report to crediting agencies, such as Experian, Equifax, and Dun & Bradstreet. This could include things such as credit cards or vendor accounts.

Matias is a serial entrepreneur and CEO of many companies that help people. He owns Superior Tradelines, LLC, which is one of the oldest and most reliable tradeline companies in the country.

Connect with me online | Email me | Call me

You have rights under the law and, unlike other companies, we tell you about them so you can exercise them. By creating an account on our website through any sign-up form or any other method, you expressly consent to Superior Tradelines, LLC, it’s employees, contractors, agents and assigns (hereinafter “our” or “we”) communicating with you, using any phone number, including a mobile or cell phone number, or email address that you have provided us using any current or future means of communication at our full discretion and transmitted by any available means. Technologies we may use to contact you include, but are not limited to, automatic telephone dialing equipment, artificial or pre-recorded voice messages, SMS text messages, or email, all of which may be transmitted by any available technology. YOU ACKNOWLEDGE THAT YOU MAY INCUR COSTS FROM YOUR SERVICE PROVIDER RELATED TO RECEIPT OF OUR COMMUNICATION AND YOU FURTHER CONSENT TO USE OF THESE MEANS OF COMMUNICATION EVEN IF YOU INCUR COSTS. You understand that you may revoke your consent to receive communication from us by visiting: https://members.superiortradelines.com/opt-out You also understand that it may take up to 48 hours before Superior Tradelines, LLC can acknowledge your revocation of consent.