Matias is a serial entrepreneur and CEO of many companies that help people. He owns Superior Tradelines, LLC, which is one of the oldest and most reliable tradeline companies in the country.

Connect with me online | Email me | Call me

I was asked to the other day, “what does a tradeline do?” It’s an interesting question, because tradelines have a definition but they also do something depending on certain circumstances. Let’s discuss both really quickly.

As we’ve explained in other articles, tradelines are accounts that appear in your credit report. It’s basically a report of your payment history inside of your credit report. This can be payment behavior on car loans, mortgages, credit cards, etc. Despite this definition, this only describes what tradelines are and not what tradelines do.

If someone is asking what trade lines do, they’re referring to the practice of piggybacking credit. Here’s what tradelines do: they impact your credit score, preferably in a good way. How do they do this? And, How do we make sure they impact your credit score in a good way?

Typically, this is achieved by adding authorized user accounts to your credit report. You inherit the history associated with those accounts. This is called piggybacking credit. If you’re added to an authorized user account with pre-existing history and positive standing, such as no missed payments as well as a high limit and low balance, it is likely to improve your credit score. We’ve studied the impact of trade lines over the years with over a thousand study participants and we’ve shown you the results on what you should expect.

Have you ever wondered why some people have excellent credit scores while others struggle to get approved for a basic loan or credit card?

The answer lies in tradelines.

What is a tradeline?

A tradeline is a credit account listed on your credit report, showing your borrowing and repayment history, also known as tradeline information.

In this article, we will explore tradelines and provide you with an in-depth understanding of what they are, how they work, and how you can create or acquire them to achieve a high credit score.

We will cover everything from the different types of tradelines to the steps involved in getting one. By the end of this article, you will have all the information you need to make informed decisions about your credit and financial future.

Let’s get started!

Tradeline defined by banks, credit bureaus, and law.

Tradelines are reflections of credit behavior. Banks define a tradeline as the financial history associated with a particular account.

The credit bureaus define a tradeline as a credit account reported on your credit file.

Legally, a credit tradeline is a piece of data on a credit report reported by the major credit bureaus, including Experian™, Equifax®, and TransUnion®.

Creditors use these details to assess creditworthiness. The accuracy of credit reports is crucial as it can significantly impact one’s life. This is why the government emphasizes and demands precision in reporting credit information.

The nature of tradelines.

Understanding tradelines goes beyond simple definitions, as they can encompass various types of credit and products.

From credit cards to mortgages, each account you open and manage becomes a tradeline. These tradelines demonstrate your borrowing and repayment history, providing valuable insight into your creditworthiness. The types of tradelines can vary widely, ranging from revolving accounts like credit cards to installment loans like car loans or student loans.

Let’s explore tradeline ownership and the different types of tradelines, as well.

The allocation of tradeline ownership can differ, resulting in various impacts on credit.

A primary tradeline denotes the original account holder. Conversely, an authorized user tradeline involves a secondary account holder that authorized to use the line of credit, but does not have repayment obligations. Furthermore, a joint tradeline is shared by multiple primary account holders, while a secured tradeline requires collateral.

All of these tradelines are reported to credit bureaus and the information associated with them can impact credit scores (positively or negatively).

The type of ownership influences the tradeline’s effect on credit. A primary tradeline has more of an impact that an authorized user tradeline. A secured tradeline has less of an impact that other types (since it reflects less of a risk).

Just as tradeline ownership can vary, so too can tradeline types.

The Different Types of Tradelines: Installment, Revolving, Open.

When it comes to lines of credit, there are different types that can impact your credit score in various ways.

An installment tradeline, such as a student loan, involves borrowing a fixed amount of money and making regular monthly payments until the loan is paid off. On the other hand, a revolving tradeline, such as a credit card account, has a credit limit and a current balance that can fluctuate based on the individual’s spending and payments. Lastly, an open tradeline, like a charge card, requires the account holder to pay the balance in full each month.

Each type contributes to the credit mix, influencing credit scores through factors such as credit utilization and the length of credit history, including available credit.

In addition to this, there are product-specific tradelines, too.

Product-specific tradelines: Auto, mortgage, business, credit card, etc.

Product-specific tradelines, such as auto loan, mortgage, business, credit card, and personal loan, cater to different financial needs.

An auto loan tradeline involves an installment credit used to finance a vehicle purchase. On the other hand, a mortgage tradeline represents a large loan amount typically used for purchasing real estate. Business tradelines are lines of credit specifically tailored for business purposes, while credit card tradelines involve revolving credit with a specified credit limit and current balance. Personal loan tradelines, on the other hand, are fixed loans that are used for personal expenses and have a set repayment plan. Each type serves a unique purpose in personal finance and has the potential to impact credit scores differently based on factors like credit utilization and monthly payments.

Creating or acquiring a tradeline.

Positive tradelines play a crucial role in impacting credit scores, while poor tradelines have a negative impact. To establish a credit history and improve credit scores, you need to demonstrate positive payment behavior.

However, there exists a catch-22 situation with tradelines: it’s challenging to acquire them without an established credit history. Therefore, obtaining tradelines becomes pivotal in building and expanding one’s credit history.

This is where managing credit tips, such as paying down balances and making timely payments, come into play, but the primary focus remains on creating or acquiring a tradeline with positive information, even for those with bad credit.

Whether it’s getting tradelines from scratch or purchasing them, the addition of tradelines with a positive payment history has shown to significantly boost credit scores, resulting in a common practice for credit score improvement.

What is a tradeline? Here are the steps to tradeline creation.

Step 1: Starting from a blank (credit) page.

For many, the first step towards building credit is requesting a credit report from one of the major credit bureaus. However, without any previous borrowing or payment activity, these reports may reveal an empty slate devoid of any credit information. This can be both frustrating and discouraging for individuals seeking to establish a financial track record.

Step 2: Starting with a starter card.

The initial step towards this endeavor typically involves applying for credit at a bank. By submitting an application, individuals open themselves up to the possibility of obtaining credit approval. However, depending on various factors like credit history or income, the bank may choose an alternate route.

In certain cases where traditional credit approval might not be possible, banks may offer individuals the option to secure a credit card by putting down a deposit. This type of credit card, known as a secured card, allows individuals to build their creditworthiness by demonstrating responsible usage and payment habits. While it may require a deposit upfront, the secured card provides an opportunity for individuals to establish and improve their credit history.

Pro tip: Getting added as an authorized user before you apply for credit is often helpful.

Step 3: Use credit and repay it.

Using your first line of credit is an important step towards building a strong financial foundation. However, it is crucial to approach it with responsible spending habits and timely repayments. By using your line of credit wisely and paying it on time, you can establish a positive credit history that will benefit you in the long run.

Step 4: Bank reports your repayment behavior.

Once you establish credit and diligently make your payments, something remarkable happens behind the scenes. The bank, serving as a silent observer, meticulously collects every bit of information related to your financial activities. Yes, every transaction, every payment made is carefully tracked. But it doesn’t stop there. This valuable treasure trove of data is then reported to the credit bureaus.

Step 5: Credit bureaus publish tradeline data in credit reports.

Once creditors have diligently reported the relevant information to credit bureaus, a crucial process unfolds – the compilation of this data into comprehensive credit reports. These credit bureaus, entrusted with the responsibility of gathering and analyzing financial information, meticulously collate all the furnished data. Subsequently, these compiled credit reports serve as a reliable repository of an individual’s credit history and financial behavior. In the event that a credit report for an individual does not already exist, credit bureaus possess the authority and capability to generate one.

Step 6: You pull a credit report and see the tradeline.

Once the information pertaining to your credit activities is reported to the credit bureaus, it undergoes a process of verification and evaluation. Once confirmed, this information is then published by the credit bureaus on your credit report.

To obtain an updated view of your credit standing, you can pull a credit report from any of the major credit bureaus. This report will reflect the updated tradeline information, allowing you to review and assess your financial history accurately.

Step 7: So, what is a tradeline? See steps 1 through 6.

Basically, the process outlined above results in a tradeline. As defined above, it’s the record of your repayment history associated with a line of credit. But, rather than a mere definition, steps 1 through 6 explain it as a process that unfolds.

Buying a tradeline.

Purchasing tradelines has become a common practice in credit score improvement. One of the only ways to “buy” tradelines is through piggybacking credit: Becoming an authorized user on a credit card.

Companies exist that coordinate this effort, listing you as an authorized user on a pre-existing line of credit that’s in good standing. You pay the company for this service, and it can have a positive impact on your credit score whether you have a credit report established or not.

Alternatively, you can ask a family member or friend to add you as an authorized user, but ensure that the tradeline is in good standing and trustworthy.

Frequently Asked Questions

How much will a tradeline boost my credit?

The impact of a tradeline on your credit score can vary depending on factors such as the tradeline’s age, credit limit, and your own credit history. The study conducted by Superior Tradelines shows the potential impacts of improving credit scores with tradelines.

How Do I Choose a Tradeline?

Considering your credit score and financial goals is crucial when choosing a tradeline. Look for one with a long and positive credit history, owned by someone who has good credit habits and makes timely payments. Opt for a tradeline with low balance and utilization rate. If you want to get a really detailed answer, consider using a tradeline and credit simulator that calculates the impact of tradelines.

What Is a Seasoned Tradeline?

A seasoned tradeline refers to a credit account with a long and positive credit history. Adding a seasoned tradeline to your credit report can help improve your credit score. These tradelines are usually owned by individuals or companies that sell them to assist others in enhancing their credit. However, it’s important to carefully research and consider the potential risks and benefits before using a seasoned tradeline service.

Conclusion

In conclusion, understanding the concept of tradelines is crucial for anyone looking to improve their credit score or establish a credit history. Tradelines play a significant role in determining your creditworthiness and can greatly impact your financial future. Whether you choose to create a tradeline from scratch or buy an existing one, it’s important to consider the various types of tradelines and their implications. Remember to always stay informed and make informed decisions when it comes to managing your credit. By taking the necessary steps to establish and maintain positive tradelines, you can set yourself up for financial success and achieve your long-term goals.

You want the best tradeline company? Of course you do. Who wouldn't? Determining the best tradeline company can be quite subjective. It can be hard to find reliable information. Despite this, we have ...

What are tradelines and how do they impact credit scores?

Tradelines are accounts on your credit report that show the history of your credit usage. They can be positive or negative and are used by lenders to assess your creditworthiness. Tradelines impact scores by influencing factors like payment history, utilization, and length of history.

Are you tired of being denied loans or credit cards? Is a poor credit score getting in the way? There’s good news for you! Tradelines may be able to help boost your credit score. But first, let’s understand what tradelines are.

There’s a lot to know about this process, so we took the time to write the following information for you. In this blog post, we will discuss different types of lines and their importance in boosting your credit score.

So buckle up and get ready to learn about how tradelines can be the key to unlocking better financial opportunities for you!

Quick tradeline fundamentals.

We want to start with a very basic understanding of what trade lines are so that the rest of this page makes sense. You can skip this section if you find it too elementary, but we would suggest taking just a moment to read through the next few paragraphs.

What is credit? It’s literally nothing. It is a made-up system that we use for banking. Lenders use this system to evaluate potential loans. Our system, however imperfect it may be, allows our lenders to be efficient.

Generally speaking, you begin to have credit as a young adult. So let’s start there. Technically, you start with a blank page. Literally, a blank page because your report will have nothing on it and may not exist at all.

Getting started with tradelines.

In order to generate a credit report, you will have to apply for an obtain a line of credit, of some sort. Typically, when you first start to establish your report, you will apply for a small credit card. Capital One hands them out like candy. Otherwise, most people start with a secured card.

Some banks, like Capital One, will give you a line even if you have a thin file, meaning you have no history with credit. Even though you have no credit, they can approve you because they trust you and the line is purely based on their trust and belief that you will pay them back in you make charged on that card. This is an unsecured line.

In cases where you are not approved, you can typically get a local bank or credit union to give you a secured card. In this case, you will secure the line by handing them cash rather than them giving you a line based on trust. This is a secured line. The difference between an unsecured and secured line is that the former is based on trust while the latter is based on pre-paying for a card.

What are tradelines in terms of reporting.

When you do this, that account and your payment history and behavior you establish with it gets reported from the creditor (i.e., the bank, etc. that gave you the line) to credit reporting agencies. These are typically referred to as the bureaus. Legally, they’re CRAs, or credit reporting agencies. They are the ones that maintain the database of information referred to as credit reports. You may recognize their names as Experian, Equifax and TransUnion.

Once you establish that account and it gets reported to the reporting agencies, a report is generated. In other words, an account on your report is a tradeline. This includes:

Credit cards

Mortgages

Auto loans

What are tradelines and how do they work?

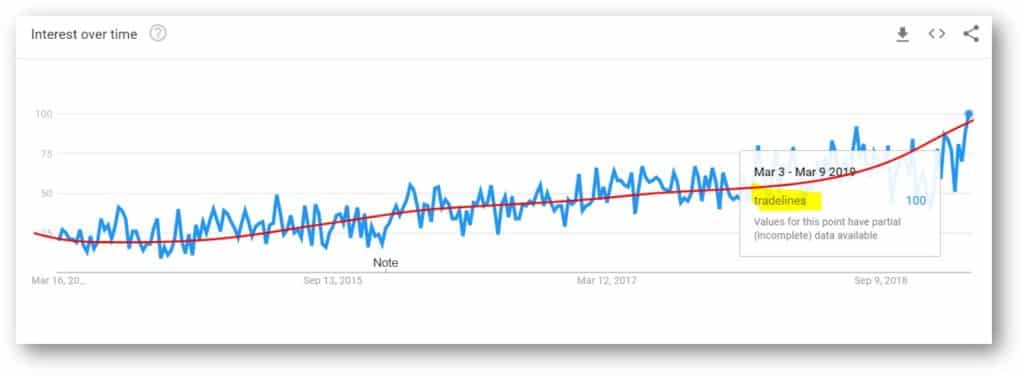

First, we should observe that the term is searched quite often. In fact, searches for the term has increased dramatically over the years. Here’s an example of Google Trends.

We all know that the definition of a tradeline is an account that appears in your report.

But, that’s not why you’re here: You’re here because you want to know what trade lines are in relation to improving your credit and being approved for some other line like a business loan or car or house.

In that regard, we are not talking generally about some previous account already appearing in your report. Instead, we are talking about adding seasoned accounts to your report for the purpose of increasing scores.

Everyone’s heard of “co-signing.” But, did you know you can share scores, too?

Here’s a quick, 60-second video to sum up the page (a longer, more thorough video, later).

Different Types of Tradelines

Those that ask “what are tradelines” might not realize that there are three main types:

Installment

Revolving

Authorized user

Installment

Installment tradelines refer to credit accounts where borrowers make regular payments over a set period. Examples include car loans and mortgages. They typically have fixed loan amounts and regular monthly payments. They play a crucial role in credit history, impacting score and utilization ratios.

Revolving

Revolving tradelines involve lines, such as credit cards. This is where the account holder is given a maximum limit to borrow against. The available credit is the difference between the limit and the current balance. This affects the utilization ratio. Maintaining a low utilization ratio on revolving account is important for a good score.

Authorized User

Authorized user tradelines are revolving accounts that the owner “authorizes” a third party to use. And, the third party (or the “authorized user”) is not responsible for repayment. Being added as an authorized user can positively impact your score.

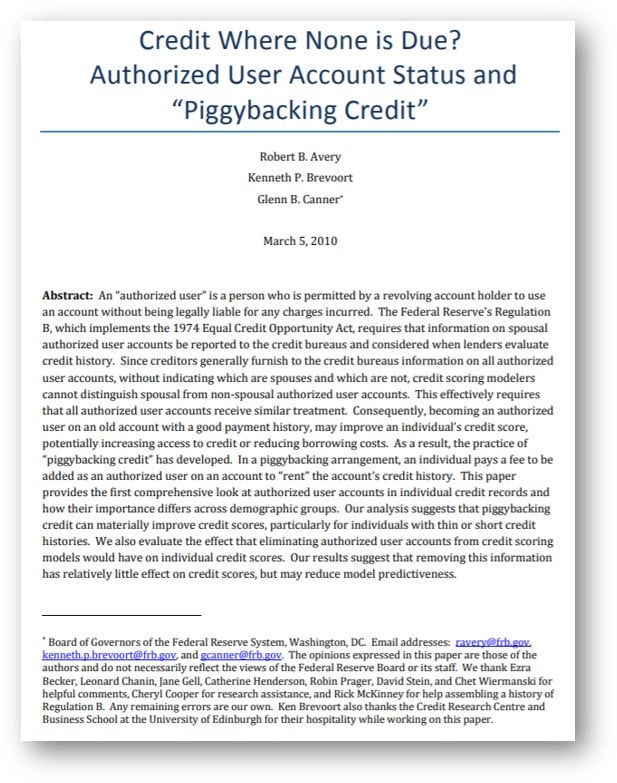

Ahe study, titled “Credit Where None Is Due,” was conducted by the Washington DC. It reviewed the practice of piggybacking. I.e., improving scores through the use of authorized user accounts. I encourage you to read just this first paragraph from the study, below.

Here’s the takeaway(s):

The law (and regulation) require that information about authorized user accounts be reported to bureaus.

Becoming an authorized user can increase the authorized user’s score.

You can buy authorized user accounts from companies and/or individuals willing to add you for a fee.

What tradelines aren’t.

What are tradelines and what they aren’t are both equally important questions. We’ve discussed tradelines, above. You should know what they are, how they help, where to get them, etc. But, what about what tradelines aren’t. That’s a horrible sentence, but an important one. Search engines are really good at showing relevant and linked content based on user searches.

If you start down the rabbit hole searching tradelines, you might end up in some pretty weird places.

In fact, you might end up in some dangerous places. So, here’s a very quick overview of some topics that we’ve discussed in detail elsewhere, but you should know about, here.

Other terms:

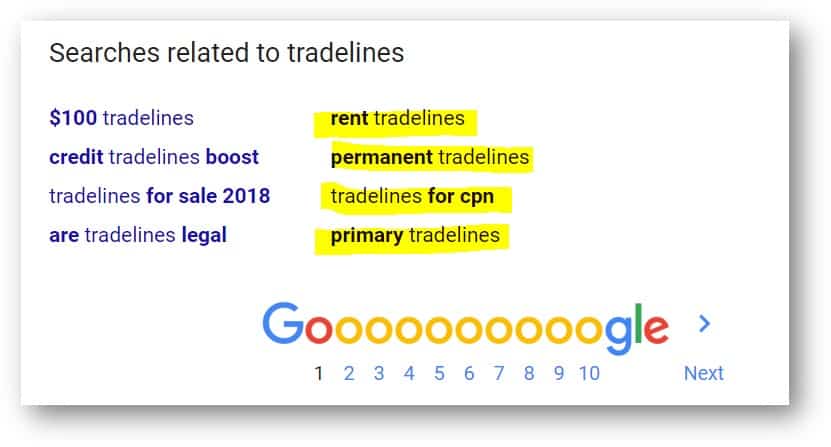

“Renting”

Renting tradelines really means two different things. In the first case, its what we’ve been talking about all along: Boosting scores by being added as an authorized user accounts. In the second case, renting tradelines mean something entirely different. There’s a new wave of companies convert your living residential rent into lines of credit.

“Permanent”

There’s no such thing as a permanent lines of credit. The only people who discuss permanent lines are those trying to rip you off. They’re just pretending to sell you something different than that which someone else would sell you.

“CPNs”

We will discuss CPNs in a different article, but suffice it to say you should stay far far away from them. It’s 100% illegal, but that’s not to say you would get prosecuted. There is more than a 0% chance of prosecuted. People are just trying to sell you a “fresh start” that doesn’t exist.

“Primary”

“Primary” is often confused with authorized user tradelines. Basically, people believe primary accounts are better than authorized users. However, you cannot buy primary line. Anyone that is suggesting they can sell you an aged primary tradeline is likely lying or misrepresenting what they are selling you.

“Business”

Business tradelines are accounts that appear in a business report. There’s no such thing as authorized user accounts for businesses. There’s no such thing as business accounts which you can purchase the boost your paydex score.

Tradelines are important.

What are tradelines in terms of the importance of credit worthiness?

They play a significant role in scoring and directly influence reported history. These lines provide detailed information about an individual’s account holder, such as the loan amount, current balance, and monthly payments. They contribute to the credit mix, which affects the utilization ratio. The presence of positive lines can boost a score, while lines that represent a negative history can have adverse consequences.

Conclusion

The question “what are tradelines” turns about to be more important and instructive than first thought. They can be a powerful tool to boost your score and improve your financial standing. By adding positive and well-managed accounts to your report, you can demonstrate responsible repayment behavior and increase your creditworthiness in the eyes of lenders. However, it is important to remember that lines are not a quick fix or a guaranteed solution. Building and maintaining good credit requires a holistic approach, including responsible borrowing, timely payments, and regular report monitoring.

There is a dramatic rise in tradeline-related searches on Reddit (and other forum-like websites). We have some opinions on that. And, we think our opinions will be helpful for consumers researching in...

You have rights under the law and, unlike other companies, we tell you about them so you can exercise them. By creating an account on our website through any sign-up form or any other method, you expressly consent to Superior Tradelines, LLC, it’s employees, contractors, agents and assigns (hereinafter “our” or “we”) communicating with you, using any phone number, including a mobile or cell phone number, or email address that you have provided us using any current or future means of communication at our full discretion and transmitted by any available means. Technologies we may use to contact you include, but are not limited to, automatic telephone dialing equipment, artificial or pre-recorded voice messages, SMS text messages, or email, all of which may be transmitted by any available technology. YOU ACKNOWLEDGE THAT YOU MAY INCUR COSTS FROM YOUR SERVICE PROVIDER RELATED TO RECEIPT OF OUR COMMUNICATION AND YOU FURTHER CONSENT TO USE OF THESE MEANS OF COMMUNICATION EVEN IF YOU INCUR COSTS. You understand that you may revoke your consent to receive communication from us by visiting: https://members.superiortradelines.com/opt-out You also understand that it may take up to 48 hours before Superior Tradelines, LLC can acknowledge your revocation of consent.